Our latest case study highlights a significant tax issue faced by many successful families –“the liquidity challenge.” Names and other key identifiers have been changed for privacy reasons, but the situation and key issues presented here are real.

Canada’s most accomplished business families have all undertaken varying levels of tax planning – and, in particular, implemented successful estate tax deferral strategies. It’s a smart and prudent way to support the enduring future of both the business and the family.

But there’s an emerging issue that is catching many families off guard.

In a nutshell: with deferral strategies in place, and as the business continues to grow, the tax liability of younger generations in the family grows exponentially. The untimely future death of a much younger family member can create a large tax liability, without the liquidity to cover it.

In the words of one family head we work with: “If our growth over the next 30 years is the same as the past 30, we’ve got a big problem.”

TROUBLE IN PARADISE

It was mid-December, just a few days before Christmas 2018. Jack Sporell stepped outside the terminal doors at Kahului Airport in Maui, took a deep breath of warm tropical air and muttered to himself, what on earth have I done?

It wasn’t the feeling he’d expected when arriving at one of the most beautiful islands on earth. Jack had travelled all around the world but, at age 80, this was his first trip to Hawaii. The journey was unique in another way too – he’d invited his three adult children and 10 grandchildren to join him. Spouses and significant others were welcome as well.

This should have been a happy occasion, but Jack was having mixed emotions for a couple of reasons:

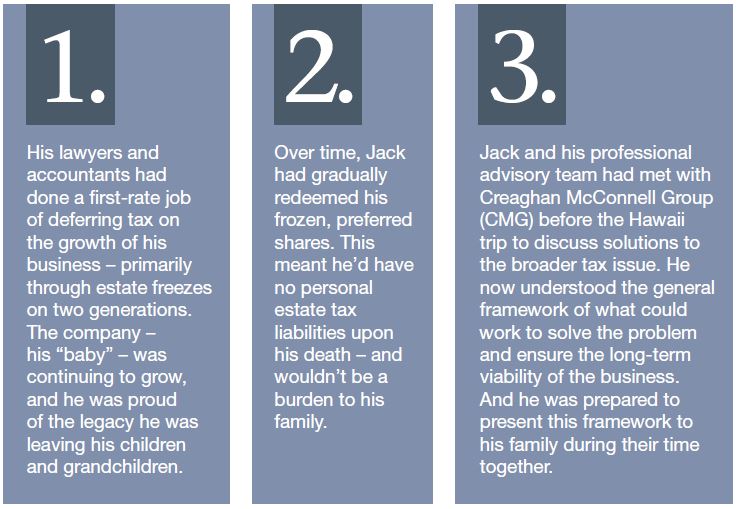

- First, a looming tax issue for the Sporell family. The Hawaii vacation wasn’t all about sun and surf. The diversified agriculture business that Jack had started nearly 50 years earlier was now worth more than $2 billion – and there were tax issues on the horizon that could impact both the future of the business and the financial security of family members. Worse, it was Jack’s use of tax deferral strategies that had put the family in this predicament. What on earth had he done indeed.

- Family communication was always sticky. The family had come together and supported Jack when his wife died five years earlier, but this was the first time since that everyone had been in one place at the same time. There were a lot of big personalities, logistical issues in getting everyone to Maui (one of the families lived in Asia, another on the U.S. west coast) and niggling conflicts that always seemed to emerge at Sporell family get togethers.

The tax issue had become apparent when an offer to buy Sporell Enterprises was tendered in 2017. It was only then that Jack and his advisors became aware of the true value of the business – and the scale of the total family tax liability emerged. Jack and his family decided not to sell, but he now knew he had a tax issue that needed to be addressed.

One of the reasons for the Maui family meeting was to discuss these issues – and the impact on the family.

Jack shook the negative thoughts from his head, quickly found the limo waiting to take him to the resort, and tried to focus on three positives:

THE TICKING TIME BOMB – HOW IT HAPPENED

One of the leading factors that drives greater (often enormous) tax liabilities for Canadian business families is the unexpected combination of successful tax deferral strategies and tremendous business growth.

Jack Sporell’s story was no exception.

He founded Sporell Enterprises in 1970 as a small start-up operation that manufactured crop fertilizer. Now, five decades later, the company was headquartered in Canada, but had spread its operations around the world. Sporell had expanded to 17 countries, manufacturing 26 different products and serving more than 45,000 clients.

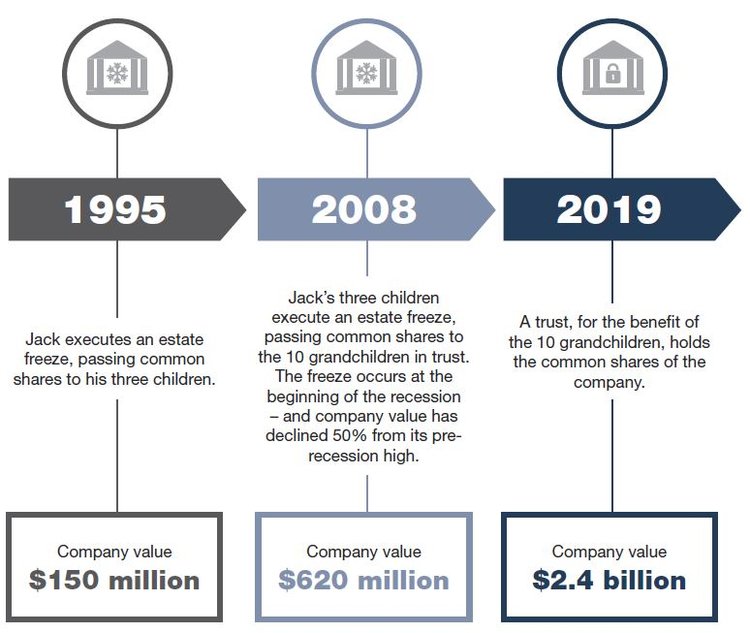

Jack and his late wife, Mariella, had three children, who were all now in their mid-to-late 50s: a daughter, Janie, with four children, and two sons, Jack Jr. and Kyle, each with three children. As part of Jack’s business planning, he had successfully deferred taxes on growth through a series of estate freeze strategies. The common shares of the company were now owned by a trust for the benefit of the third generation – Jack’s grandchildren.

None of Jack’s three children or 10 grandchildren were actively involved in the day-to-day management of the company, and Jack himself retired from active management duties 15 years ago. But the company was still privately-held and Jack’s children anticipated that one or more of the grandchildren would eventually become active in the business given their interests and current career paths. In any case, Jack was grooming his family to be competent owners and directors. It was a key reason why Jack’s family rejected the takeover offer in 2017.

ESTATE FREEZES IN THE SPORELL FAMILY AND SPORELL ENTERPRISES

As the accompanying chart demonstrates, much of the value of Sporell Enterprises had been generated in the previous 10 years with some explosive growth. While the growth story was impressive, the potential ticking tax bomb was troubling. The third-generation grandchildren would inherit a huge tax liability with their common shares in a trust.

Here’s specifically what the family was up against:

- The tax. Through the 2008 trust, each grandchild was entitled to shares valued at $240 million. These shares carried a capital gains tax liability of approximately $60 million each, based on current capital gains tax rates. While the trust was in place, capital gains would remain deferred. If one of the grandchildren were to die, there would be no tax impact. The shares would remain in the trust to be divided among remaining beneficiaries, with no capital gains liability realized.

- The end of the trust. Under tax rules, the trust effectively had a life of 21 years, or until 2029. Before that date, the family planned to transfer shares to each beneficiary grandchild on a tax-deferred basis. The common shares would then be held by each grandchild directly.

- The potential liquidity need. Here’s where the tax issue emerges. Should a capital gains liability be realized for any grandchild (upon death, for example), their estate would need a $60 million dividend to cover the tax liability. Without adequate planning, the family would be looking at the payment of a $600 million dividend.

- The threat to the business. Sporell Enterprises had never been a particularly liquid asset, with most cash invested back in operations and real estate. The sudden need for liquidity would require the sale of some or all of the business – and under conditions that might not be ideal for realizing its full value. The Sporells were now realizing that a single unfortunate event (an unexpected death), combined with a lack of planning, could conceivably destroy a business dynasty that had lasted three generations. It was not what they wanted.

“The sudden need for liquidity would require the sale of some or all of the business – and under conditions that might not be ideal for realizing its full value.”

BEACHSIDE – OUTLINING A SOLUTION

The Four Seasons had always been Jack’s hotel of choice when travelling, and the resort in Maui didn’t disappoint. He’d chosen Hawaii because of its central location, reducing the flight time for family members living in Asia and California, and fulfilling a bucket list destination for himself.

He’d also hoped that the gentle “Hawaiian vibe” would reduce family strains and offer an inspiring location where family members could leave their other life issues behind and focus on a solution for the business problem at hand.

The results exceeded Jack’s expectations.

With his grandchildren already in (or approaching) adulthood, and Jack’s own children reaching the end of middle age, the family rivalries had mellowed. There was a greater appreciation for the role of Sporell Enterprises in their lives, and what it provided them.

On top of all of this, with the older grandchildren showing an interest in taking active roles in the business, the youngest generation was leaning in to the conversation about the tax issue and potential solutions. The younger folk were engaged.

Based on CMG’s proposed solution, Jack’s longest-serving and most trusted lawyer took the family through the highlights.

The solution consisted of:

This was the part of the solution that Jack was most concerned about, as it involved educating the next generation about the need to allocate a portion of the dividend cashflow to fund some of the tax liability, instead of their own lifestyles. In essence, it meant putting some money away instead of spending it all. It could be a tricky conversation, but the need was clearly explained. The reallocated dividends would stay in the business and still be family assets.

In the end, the Sporell family members agreed that the strategy of slowly building liquidity in this manner would have a marginal impact on their lifestyles – and ensure the family business survived intact, without a need to sell off any key assets in the company.

Through an “insured refreeze” strategy, Jack’s lawyer and CMG set out a solution which allowed for the purchase of permanent life insurance protection (to match the eventual liquidity need) at little ongoing cash cost. This insurance strategy was the cornerstone of the solution, and ensured there would always be liquid assets to match the potential tax liability, even as the liability grew over time.

This gave Jack and his entire family peace of mind. They had the addressed the inevitable tax issue with a proactive plan for liquidity.

SAFEGUARDING THE BUSINESS AND THE FAMILY

With the business side of the trip completed, Jack and his family did something that they rarely had a chance to do – enjoy a week of great meals, adventures, and fun as a family. When Jack returned to his home north of Toronto, he gave instructions to begin putting the solution in place.

Turns out, some of that soothing Hawaiian vibe had followed Jack home.

He’d always been proud of the growth in his business, and in managing the tax deferral strategies for himself and his children. But Jack was particularly proud of his latest actions – safeguarding the long-term viability of his business, his baby, protecting the wealth of the Sporell family’s youngest generation, and engaging all members of the family in Maui so they understood and supported the plan.