Here’s an issue that we see frequently with business families.

As a business owner grows the family business, the issue of financial security for the “non-active spouse” often emerges. This is especially true as plans are made to transition the business to the next generation.

For successful business families, it’s an issue that’s rarely about money and net worth and almost always about autonomy and control. Few non-active spouses want to step into the shoes of the business owner if the “owner spouse” dies first. They’ve typically had little or no active role in the business throughout their relationship, and most non-active spouses don’t want to take on an active role in the later stages of their life. They don’t want to be sitting in a boardroom making key business decisions. It’s not what they want.

So what do they want? What are they really concerned about?

What we often see in working with business families is that it comes down to spousal security – but what does that even mean? In our experience, it’s essential to talk through what it means, and to not miss this important conversation. Taking care of the non-active spouse’s autonomy and independence avoids a lot of problems later on.

Starting the conversation typically involves three concerns for the spouse.

It’s especially important to identify their desired role should the owner/founder spouse die first. Specifically, the non-active spouse will have some variation of three questions on their mind:

- What am I responsible for going forward? What’s expected of me?

- Who is in control of my financial future?

- Is anyone in control of me? (This question always reminds us of one family situation where the spouse wanted to purchase a three-bedroom condo, but her children suggested she only needed two bedrooms. When relating this story to another family we were working with, the spouse simply said, “Please don’t let that happen to me.”)

Once these concerns are discussed – and the questions answered – planning can commence for truly satisfying the spouse’s concerns. This includes assessing the available options for structuring the right plan and which assets to use in funding it. There are many ways to achieve spousal security. Insurance is one (and not the only) structure to consider.

The case study that follows highlights the solution undertaken by one family. While details have been changed to protect their identify, the circumstances and the solution are real.

CASE STUDY:

LIFE INSURANCE AS A PRACTICAL SOLUTION FOR SPOUSAL SECURITY

A lifetime of hard work had paid off for Ted and Patricia Harding. Ted had taken over his father’s single manufacturing plant in 1985. Over the next 35 years, he had turned it into a diversified, global business conglomerate, 100 times the size of the business he’d inherited from his father. He and Patricia had also raised three children – now all in their 30s and playing active roles in the business.

The Hardings felt blessed.

Patricia had run the household – and was instrumental in guiding Ted on his most important business decisions. She had also led the charge in raising millions of dollars for Toronto homeless shelters. Her father had suffered from mental illness and left home when she was young. He had used the shelter system. This had a lasting impact on Patricia, and her charity work remained a big part of her life. Her drive to improve the lives of the city’s most vulnerable was relentless.

LETTING GO OF THE REINS

Ted was now 67 and easing himself out of day-to-day operations. The children were growing into admiral stewards of the business. But there were risks ahead. The family was beginning a lengthy business review, looking to sell certain businesses and modernize others. Ted had faith in both the plans and in his children – and also knew there were sure to be ups and downs along the way.

As part of the business review, the Harding family office had begun to revisit the estate plans for Ted and Patricia. Of particular concern was ensuring financial security for Patricia in the event that Ted pre-deceased her. She was only 62 and in excellent health. The couple was realistic in recognizing the actuarial probabilities: Patricia was five years younger and would likely outlive her husband by a decade or more.

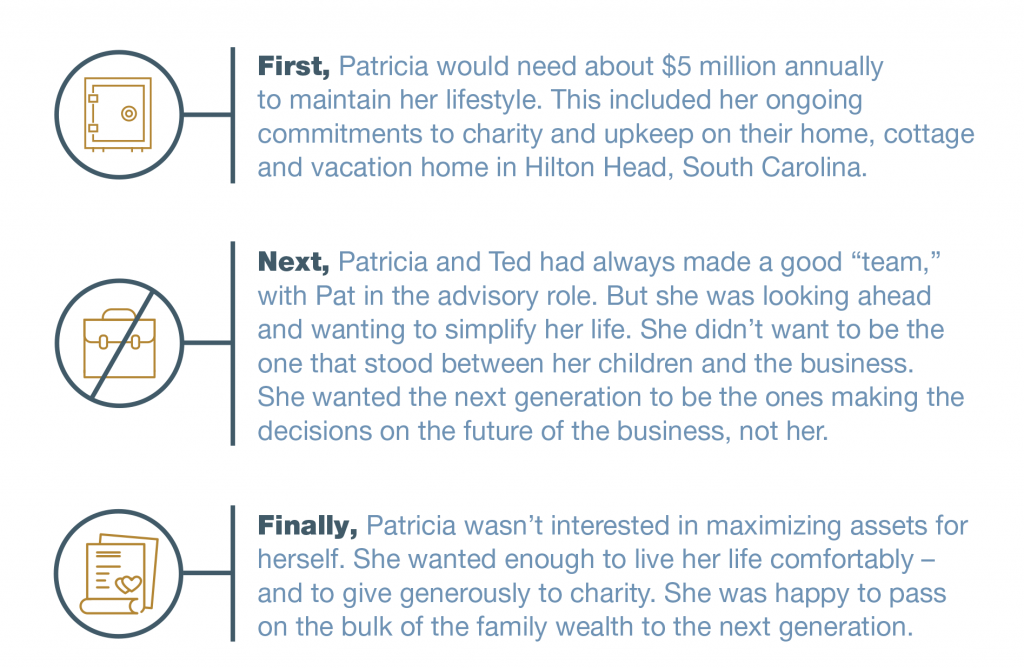

Kathleen Hodgson had run the Harding family office for 15 years. She was tasked with renewing the plan – one that Ted, Patricia and their children could agree on. In working with Patricia during the planning process, Kathleen arrived at three conclusions:

BUILDING THE SPOUSAL SECURITY PLAN

Kathleen estimated Patricia would need a nest egg of about $200 million to ensure her lifestyle needs. She talked to the family about severing one of the business assets and earmarking it specifically for Patricia. The rental income from a large manufacturing plant owned by the business in British Columbia seemed like an ideal fit. It generated a consistent stream of income that would cover Patricia’s annual expenses.

But there were two roadblocks. The Hardings’ tax lawyers advised that divesting the B.C. plant from the family holdings was possible, and also complex. Patricia was resistant. She didn’t want to own (or manage) a large plant – especially when she knew it was an important part of the business, and especially not in the later years of her life, she wanted to focus more of her energy on charitable work. Besides, she wanted her kids to be the ones making the key business decisions going forward.

While the Hardings could sell the plant, it would mean paying tax on the sale and losing a valuable business asset. And it was also premature – the family likely wouldn’t need the liquidity for Patricia for many years to come.

Kathleen needed an alternative strategy.

This led to a meeting with specialist advisors to business families. Kathleen outlined Patricia’s needs and the issues involved. After reviewing the various alternatives, a solution emerged that no one thought could be applicable to such a wealthy family like the Hardings: life insurance. After all, why do wealthy families need life insurance? They don’t. But it also doesn’t mean that life insurance isn’t useful to them.

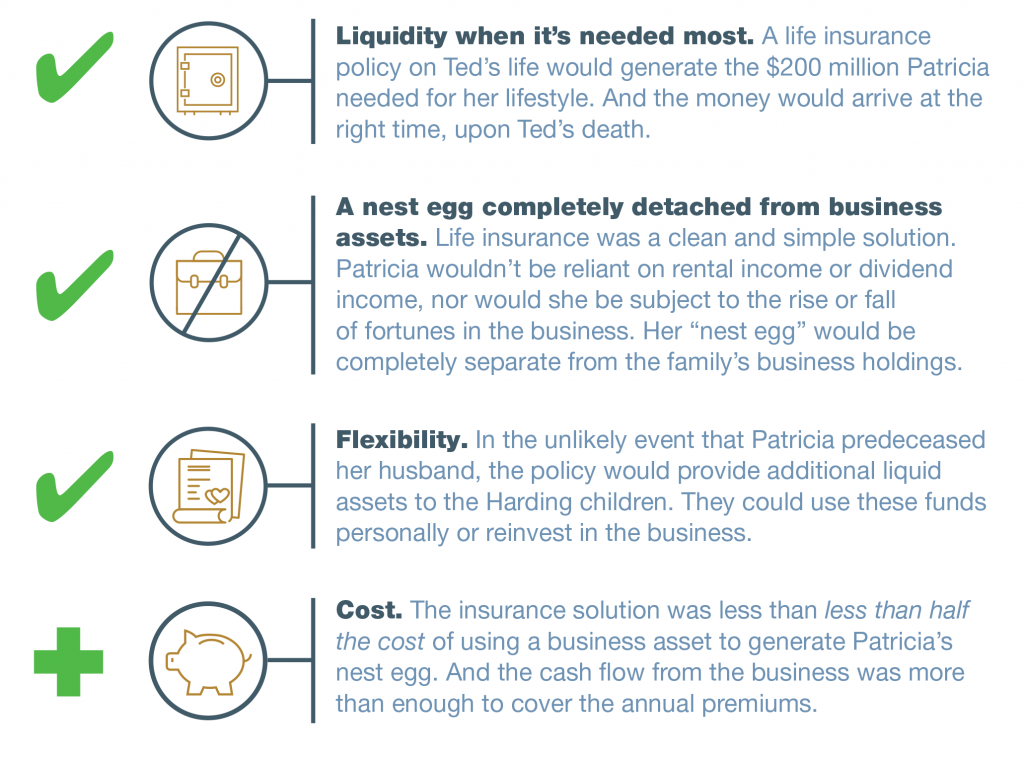

The advantages of this approach soon became apparent:

PUTTING THE STRATEGY IN PLACE

Kathleen went back to the Hardings and presented the plan. It ticked all the boxes for each of the stakeholders. Ted and the children were relieved that business assets would remain untouched. Over the short-term, the family would direct some business dividends to the insurance premiums as a necessary investment in Patricia’s future security. The plan also provided liquidity that would eventually be passed down to the children after both parents were gone.

For Patricia, the insurance solution gave her everything she needed. It simplified her financial affairs in her later years. It gave her the money she needed to live the lifestyle that she and Ted had carefully built. And just as importantly, it let her continue her charitable work and legacy.

The Hardings had been looking for ways to protect both Patricia and the business for the future. Having a sound plan enabled them to look at life insurance as a funding solution – and it actually ticked all of the boxes.

Download and view this story as a PDF:

Paul Russell is a freelance writer based in Toronto.